As a property investor, one of the biggest decisions you will make is the location and property type that you choose to invest in. Factors such as the price of the property, the achievable rental income and whether the property is likely to have strong value growth will all contribute towards the returns on your investment.

Why Mansfield is a promising location for property investment

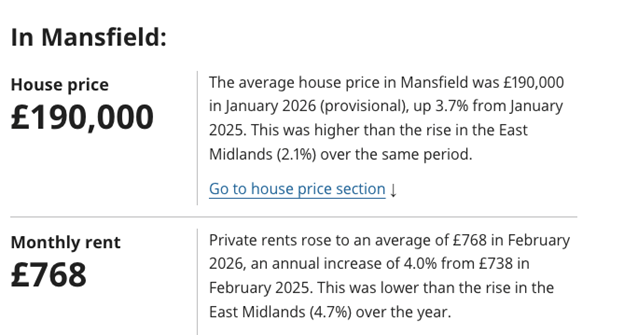

Nottingham is one of the fastest growing areas for Buy to Let investments and areas such as Mansfield offer lower than average house prices. In January 2026, the average house price in Mansfield was £190,000, with an average monthly rent of £768.

Source: ons.gov.uk

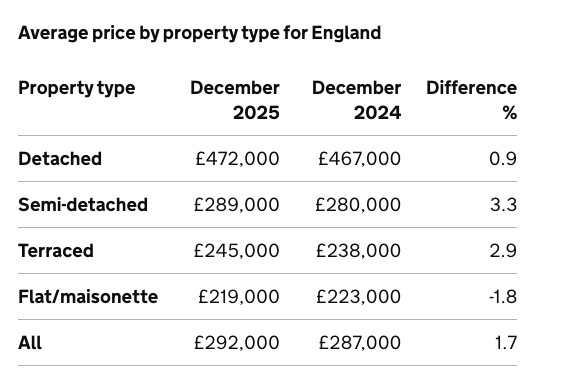

Compared to the national average house price for England, which was £292,000, investors can buy property in Mansfield for around £100,000 less.

Source: UK House Price Index for December 2025

Therefore, buying property with a mortgage in Mansfield is ideal for investors who are looking to pay less upfront costs. With stamp duty tax surcharges to pay, buying cheaper property also minimises this cost.

Regeneration projects can have a significant effect on house price growth and Mansfield has recently been granted £20 million in government funding to improve infrastructure and to improve the town centre.

Buy to Let vs residential mortgages in Mansfield

Mortgage interest rates for Buy to Let mortgages in Mansfield are generally higher than residential mortgages, due to the additional risk perceived by lenders.

Another key difference is that investors will usually require a higher deposit of between 20% and 40%, while deposit requirements for residential mortgages can be as low as 5% to 10%. Lenders will typically want to ensure that the rental income will comfortably cover the mortgage payments, with many requiring at least 125% rental income coverage.

Buy to Let mortgages are most commonly interest-only, where the investor pays off the capital at the end of the mortgage term. The majority of residential mortgages are taken out on a capital and interest repayment basis, so the property is owned by the end of the term.